LexNow, la base de données juridique du Luxembourg

Une plateforme unique réunissant le droit fiscal, le droit social, le corporate, IP/ IT, le droit civil, le droit du secteur des fonds d’investissement, le droit du secteur immobilier et le Data Privacy, augmentée par la puissance de LexGAIN, la solution d'intelligence artificielle conçue par Legitech.

Droit fiscal

En savoir plusCorporate

Droit social & LEXPRH

En savoir plusFonds d'investissement

En savoir plusData Privacy

En savoir plusDroit immobilier

En savoir plus

LexNow, c'est tout le savoir de Legitech et de ses auteurs réuni en une seule et même solution en ligne.

Un moteur de recherche performant et intuitif permettant un accès rapide et complet à la législation consolidée, la jurisprudence y relative (textes in extenso), les dossiers parlementaires, les circulaires, ainsi que des commentaires et notes rédigés par des professionnels de renom en droit fiscal, droit social, droit des sociétés et du secteur financier.

Une mise à jour permanente.

Recherchez parmi une vaste base de données

Plus de

56 000

décisions jurisprudentielles

Plus de

6 600

documents parlementaires

Plus de

4 400

textes législatifs

Plus de

1 400

circulaires

Plus de

15 000

doctrines

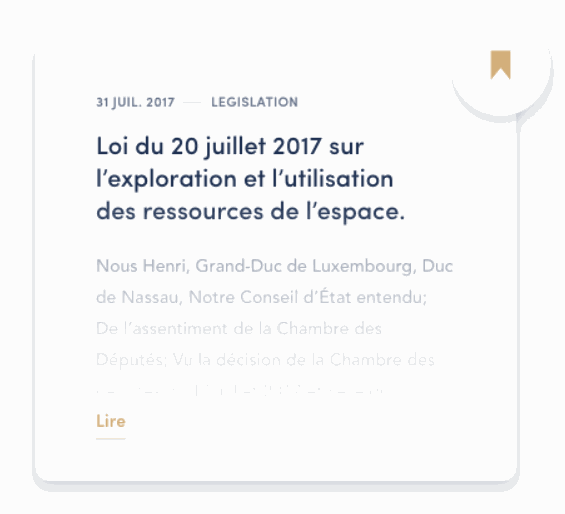

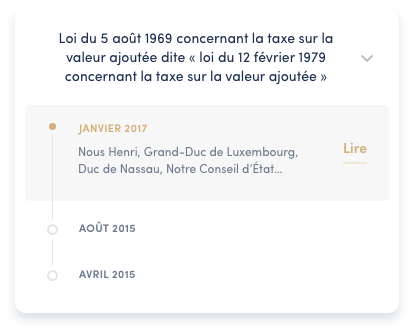

Accédez à l’historique de la législation grâce au « versioning »

Retrouvez aisément vos documents favoris